One World, One (Healthcare) problem: How the Swiss create market discipline

Discipline: good for your goals and your healthcare systems!

Improving health is a universal goal, but equally universal are challenges to providing care in a modern health care system. Switzerland lays claim to the highest life expectancy in Europe,[1] at 84 years. This is five years longer than even pre-pandemic U.S. life expectancy. Today, we end our series on international systems by examining what contributes to Switzerland’s success.

(Check out the rest of the series: How Canada sidesteps having insurance markets spiral to only cover the sickest patients; How the UK tackles the tough problem of information, and Germany as a Choice Meister.)

1. Discipline: Good for your resolutions AND your healthcare markets

Providing universal healthcare coverage is daunting and expensive. A common crutch for this conundrum is: ummm, can we just make it the government’s problem? Canada and the UK have gone this common route. However, there are two disadvantages to this solution. First, high quality administration is not a key strength of governments-- think creating enforceable guidelines and laws, not managing thousands of dynamic negotiations and prices. The Bill of Rights is a great document, guiding the actions of a nation. In contrast, most DMVs, who are processing thousands of applications and payments daily-- not so amazing.

More importantly, nationalized health systems lose the benefits of consumer choice and competition. A huge frustration in healthcare is that people feel they have no choice in one of their most high-stakes purchases. When consumers can choose between businesses, this creates discipline on these businesses. For example, have you ever tried to call your local electricity provider—a legal monopoly in most places—with a complaint or to request a quick solution to a downed line? How did the power company respond compared to a local restaurant and a negative Google review? Or the lenient return policies from retailers with plenty of competition, such as Target? Any business subject to competition and negative word of mouth, be it an Etsy business or your local heating and air company, is more likely to rush to rectify your problem, lest they lose future business.

The hang-up with using the private sector is that some groups end up not being able to afford insurance, so most countries decide some, if not all, insurance must be created and provided by the government. Is there a way to allow private insurers to provide choice to citizens and discipline to plan offerings, yet still provide coverage to all citizens?

2. An individual mandate? Yes, that’s vaguely familiar…

The Swiss have decided, “Yes!”: all health insurance in Switzerland is provided by private nonprofit insurers. Buying insurance is mandatory for all citizens, via an “individual mandate.” If this sounds familiar, the Swiss system was a model for the ACA reforms. (I briefly explain the ACA version here.) However, U.S. citizens sort into several different markets: employer-sponsored insurance, Medicare, Medicaid, and, finally, the individual market for purchasing an individual plan—where the ACA’s individual mandate was most relevant. This is a much smaller market (less than 6 percent of U.S. insurance enrollment) and generally the last resort if you can’t obtain coverage from the first three.[2] What is markedly different about the Swiss system is that the individual mandate applies to all citizens and all citizens purchase their plan the same market. Switzerland mitigates the problem of adverse selection (generous plans attracting many sick people) by keeping the insurance pool large, which also encourages more insurers to participate.[3]

Standard covered services are chosen by the government, but plans are offered over three age ranges with 6 different deductible choices. Besides deductibles, the most relevant dimension of consumer choice is how a consumer chooses their doctors. The basic plan offers free choice of any doctor. However, consumers can choose lower premiums for tradeoffs in how they access care, i.e. by using gatekeeping primary care physicians or other types of HMO-style restricted access.

The final hang-up of disadvantaged groups is solved by premium subsidies. Almost a third of citizens, 27.3 percent, qualified for these subsidies in 2016. Maternity care is mandated to be fully covered, as well as some preventive care, and children’s policies have no cost sharing. In this way, social safety nets exist, even within private sector insurance.

3. Gains from discipline, healthcare markets version

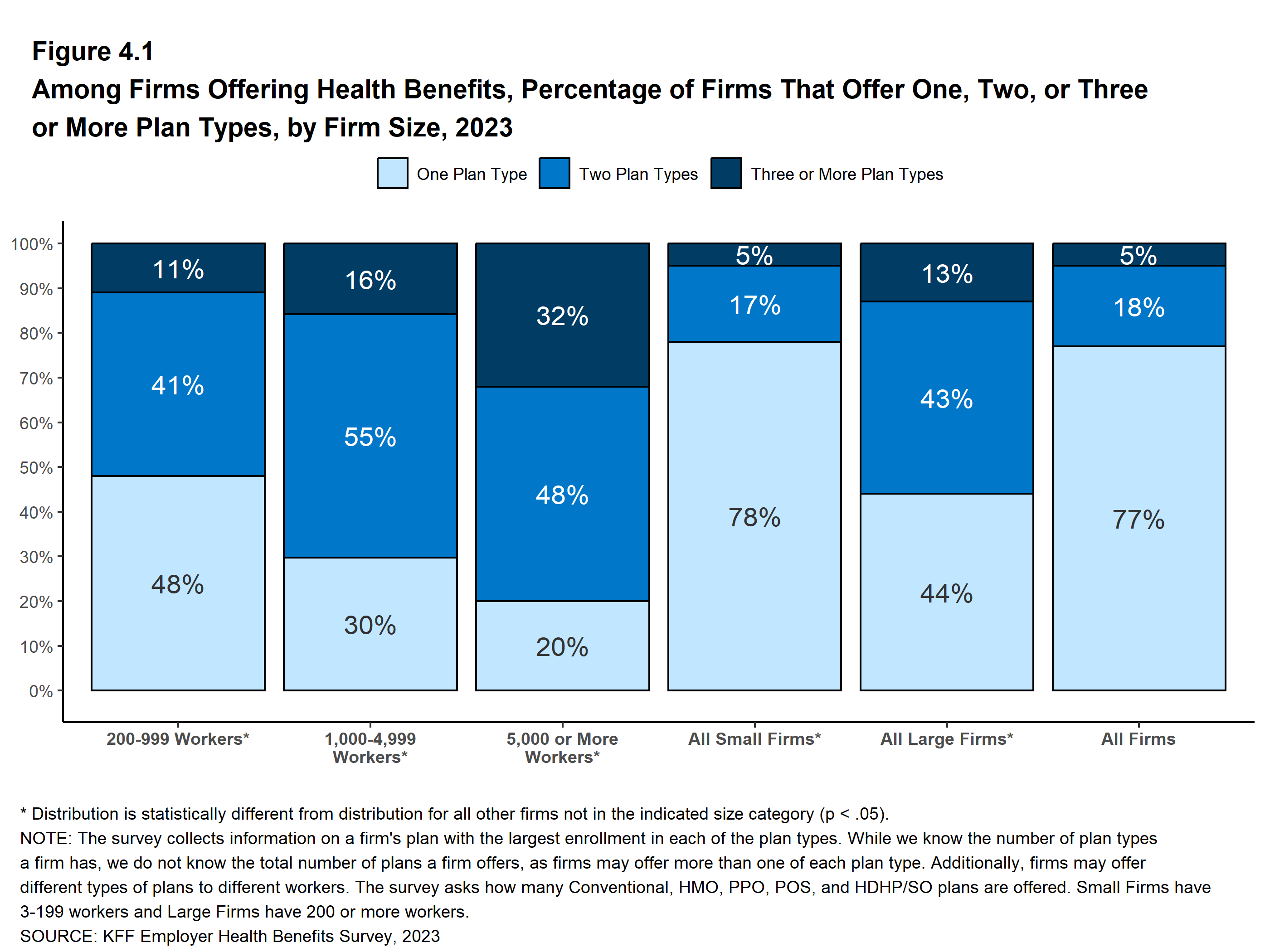

Although the range of plan choices is somewhat narrow, the market discipline it introduces is still of interest. The Swiss government sets coverage standards and deductible choices, but these can range from 248 USD up to 2,066 USD (2016).[4] Note that even this limited choice is more than most people have in the U.S.! Under employer-based insurance (approximately 80 percent of U.S. private insurance), 77 percent of firms offering health benefits offer only one type of health plan.[5] Even at the employer-purchase level, market discipline is weak because the employer’s costs of switching administrative systems is high, and employers certainly can’t change a plan covering hundreds of people based on individual employee preferences.

Switzerland’s experience is a resounding validation of the desire for choice.[6] Over 65 percent of citizens chose a plan different than the standard basic coverage plan with free physician choice.[7] The Swiss system performs quite well on physician interactions, the most salient choice dimension among plans (and thus, the most promising area for competition to discipline competing plans). Fewer than 10 percent of adults reported waiting longer than 2 months to see a specialist, in contrast to 30 percent of adults using fully-government provided care in Canada. The Swiss also performed well on hearing back from their doctor the same day (some plan choices focus on telehealth) and in the ability of chronic care patients to discuss care with their doctors.[8] While the Swiss choice to use private insurers rather than the government may be unusual in modern systems, its potential for leveraging choice and market discipline leaves plenty to explore.

[1] Our World in Data, “Life Expectancy.” Maybe tied with Iceland in 2023, but ahead for the past few years.

[2] The ACA Marketplace enrollment was 18.2 million in 2023. (KFF, “As ACA Marketplace Enrollment Reaches Record High, Fewer Are Buying Individual Market Coverage Elsewhere” Sept 7, 2023). In comparison, employer-sponsored insurance covered 155 million nonelderly people in 2019. (KFF, “2021 Employer Health Benefits Survey”). Total U.S. health insurance enrollment was 304 million in 2023. (Census, “Health Insurance Coverage in the United States: 2022”, Sept 12, 2023.).

[3] The Swiss system also features a risk-adjusted cost reallocation system, where funds collected from premiums are moved from insurers who ended up with a less-sick population and given to insurers who ended up with a sicker population, on average. Germany uses a similar system to respond to adverse selection in insurance markets.

[4] Tikkanen et al. “Switzerland” International Health Care System Profiles, June 5, 2020. Commonwealth Fund.

[5] Kaiser Family Foundation, “2023 Employer Health Benefits Survey. Section 4: Types of Plans Offered” Figure 4.1.

{kind=link}

[6] Let the desire for choice resound across health care debates like an echoing yodel through the Alps!

[7] Tikkanen et al. “Switzerland” International Health Care System Profiles, June 5, 2020. Commonwealth Fund.

[8] In New Survey Of Eleven Countries, US Adults Still Struggle With Access To And Affordability Of Health Care Robin Osborn, David Squires, Michelle M. Doty, Dana O. Sarnak, and Eric C. Schneider. Health Affairs 2016 35:12, 2327-2336