One World, One (Healthcare) Problem: How Germany Enables Choice

Rice and beans, cellphones, and how to become a Meister of insurance choice

One World, One (Healthcare) Problem: How Germany Enables Choice

Improving health is a universal goal, but equally universal are the challenges to providing this care in a modern health care system. In this series, we’ll examine a problem faced by every healthcare system and highlight one country that effectively solves it. We’ve seen how Canada sidesteps having insurance markets spiral to only cover the sickest patients and how the UK tackles the tough problem of information. Today, how Germany introduces choice into universal coverage.

1. Problem: Giving everyone the same thing is bad; choice is good

Anyone grow up with school uniforms? Or matching sibling outfits? Did it ever make you feel like the young man pictured below? Or how would you like your food to be fully provided, but only be served rice and beans? (Mom says its healthy…) In general, people prefer some choice in their lives- what to wear, what to eat, where to live.

Sometimes the quest for universal healthcare can run up against the ability to choose. For example, Canada provides the same care to all citizens, equally affordable, but the downside of this system is that, instead of paying in money, people often end up “paying” in time—Canada is known for its long wait times for care.[1]

In the non-healthcare parts of our lives, people choose differently based on their own needs and their own preferences. Think about the variety of cell phones out there. If all you want is to call your Mom and take some pictures, you’re fine with the basic model. There’s even a resurgence of the “dumb” flip phone for trendy digital minimalists![2] But some folks might be running their businesses off their phones, or enjoy the latest apps, and they’re willing to pay up (significantly) for the latest models with the fastest connectivity.

Depriving consumers of choice in their health care plans is inefficient because some end up with more coverage than they want (which either they or the government is paying for!), whereas some people want more—and they’d be willing to pay for it.

2. Germany’s Choice Compromise

The German health care system has two parts: a mandatory insurance system called “Sickness Funds” and a smaller private insurance industry that acts as both a substitute and a supplement to Sickness Funds.

The first pillar of the German health care approach sounds familiar: Funding is through employer and employee contributions. However, beyond this, the US and German systems diverge. In the US, insurance is commonly provided by employers, but is only mandated (post-ACA) for firms of 50 full-time employees and higher. To provide this insurance, a U.S. employer must contract individually with an insurer. This means an employee has limited choices of plans- for logistical and financial reasons it’s not feasible for employers to contract with multiple insurers.

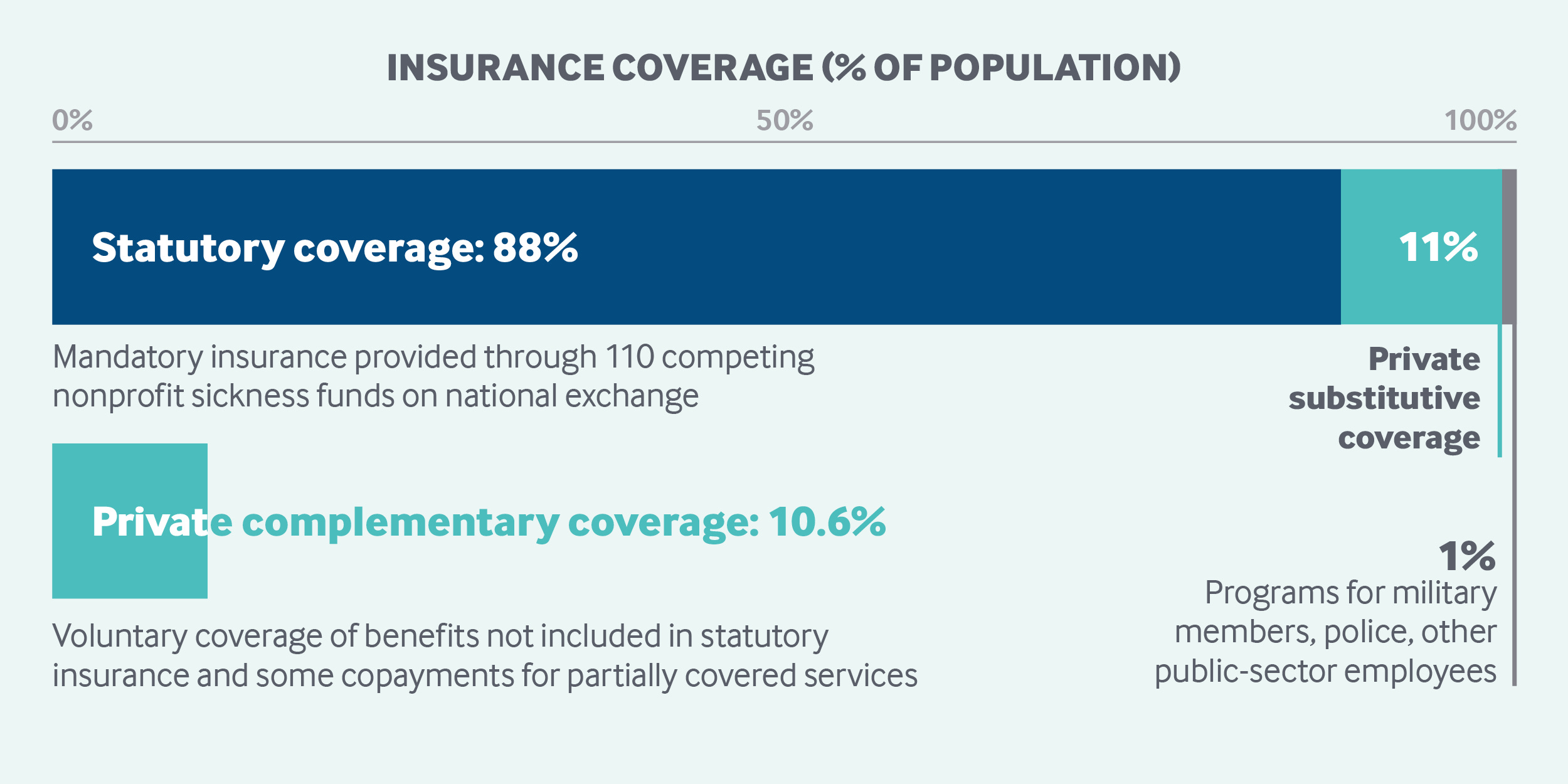

In the German system, mandated employer/employee wage contributions are collected, but then pooled centrally to fund what are called “Sickness Funds.” Sickness funds are a large set (110 in 2023) of nongovernmental insurance plans which must cover a comprehensive set of services. Wage contributions are allocated to the Sickness Funds based on risk-adjusted capitation. This means each fund is paid according to how many members it enrolls, while also adjusting for how sick that fund’s enrollees are. This adjustment is to address the adverse selection problem, where sicker people will choose different plans in the system. (See the Canadian discussion in this series). There is a federal plan for those that are unemployed.

Individuals beyond a certain income threshold can opt to leave the Sickness Fund system and enroll in private insurance, which offers a more extensive range of services. Private insurance is also available to provide supplementary services outside those mandated for Sickness Funds.

3. How this solves the bad and promotes the good

There are at least two ways the German health care system promotes plenty of choice. First, the default Sickness Fund enrollment offers over 100 plans to choose from. These plans compete for enrollees by offering a range of deductibles and no-claims bonuses—if you don’t use care that year, you get a rebate! This encourages preventive care, or at least attracts those that are already engaged in prevention to choose a plan that pays them back for their lifestyle choices.[3]

Second, just like some people choose to suffer through phones without access to cat memes but some pay up for more, the combination of Sickness Funds plus private insurance allows consumers who want more to buy different coverage. About 88 percent of the German population are enrolled in Sickness Funds, but 11 percent choose private insurance instead.[4] Private insurance is also used as a supplement. Germans can buy private insurance for minor benefits not covered by Sickness Funds, such as private hospital rooms. Additionally, physicians can offer services outside of the mandated coverage for out-of-pocket payments from patients.

Beyond the monotony of rice and beans, Germans may urge you to try some Kartoffelsalat or Sauerkraut. Perhaps we can learn some other healthy choices from their health care system!

As always, keep me updated on what you’re up to or reach out to chat with me about these issues!

Read the others in this series: Canada deftly avoids the death spiral, Germany is a meister of choice, and Switzerland’s markets of plenty.

Best,

TMD

[1] In a survey by the Commonwealth Fund in 2016, Canadians faced the longest wait times of patients in 11 countries.

[2] I’m not making this up, Fast Company and CNBC say so.

[3] The amazing (and German) director of my Roots of Progress Fellowship, Heike Larson, has written a nice piece on this idea called “Why is there a “safe driving” discount on car insurance, but not a “healthy living” discount for health insurance?”

[4] The Commonwealth Fund, “International Health Care System Profiles: Germany” June 5, 2020.