Disentangling Drug Prices: Is insurance friend or foe? (Part III)

The Inflation Reduction Act and I dare to ask: should drugs even be in insurance??

In Part I, we learned that final pharmaceutical prices result from a multi-tiered layer cake. Last month’s layer, the Pharmacy Benefit Managers (or PBMs), may use their extranormal market power to encourage cost-efficient drug use, or maybe just make a gooey PBJ mess of hidden prices and rebates. (Think I was hungry while writing this series?). Today, how does the top layer, insurance, fit into the picture?

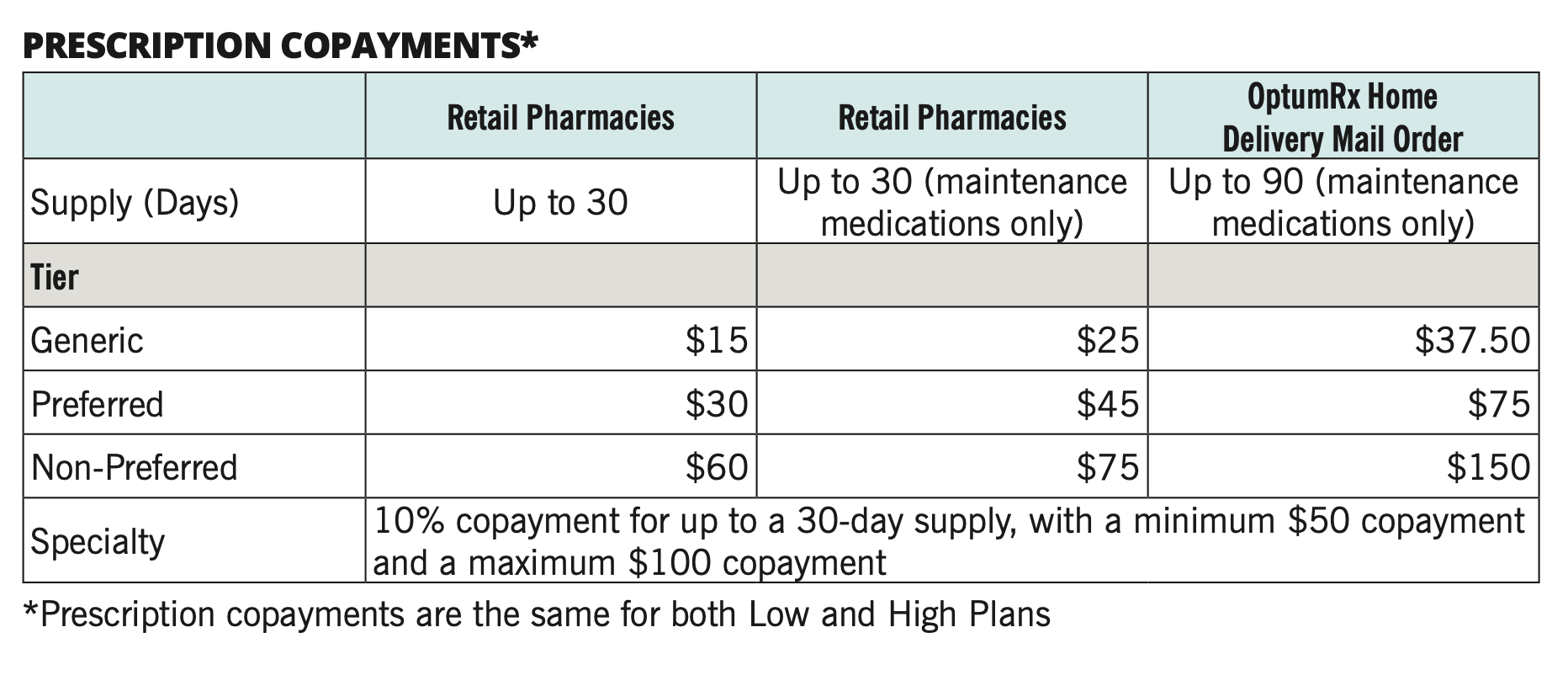

1. Preferred, More Preferred, Most Preferred

If your pharma out-of-pocket costs are all over the place, one reason is likely how insurance covers them. Not all drugs are viewed equally and, just like in a high school drama, the mean girls -insurers- force them into cliques, called “tiers.” Tiers are roughly built around the cost of the drug, but also function as a bargaining chip to force lower prices from a drug manufacturer. “Keep your prices down, or you’re out of the popular clique!”

What’s the popular clique? The cheapest tier, of course! For the patient, tiers correspond to copay levels. Patient copays increase up the tiers. Usually, the cheapest copay tier is generic drugs, followed by a Preferred Brand tier of brand name drugs where the insurer has negotiated better rates. A typical third tier is Non-Preferred Branded drugs- perhaps brands with an existing generic substitute. Finally, the last tier is for the most expensive drugs, such as cancer drugs or biologics. To account for the especially high prices in this tier, patients commonly pay a percentage of the drug price, rather than a fixed copay.

2. Inflation Reduction Act Forecast: High and rising.

Drug prices have been high and rising for years, but we’re especially feeling the pinch with economy-wide inflation levels steadily cracking 5-9% over the past year. Besides monetary policy attempts to pull back rising prices, the Inflation Reduction Act of 2022 included several carve outs aimed at pharmaceuticals.

In particular, the Act requires the federal government to negotiate prices for drugs with the highest spending levels in Medicare Part D (see my post explaining Part D here) and requires drug manufacturers to return rebates to Medicare if prices rise faster than inflation. It also attempts to reduce patient costs (I’d say shortsightedly, see point 3) by imposing a $2,000 limit on yearly out-of-pocket spending for Medicare enrollees and limits cost sharing for insulin to $35 per month.[1] (A reminder why attempting to freeze prices just pushes the problem down the road.)

3. Question everything: Why are chronic drugs even involved in insurance?

Before we end discussion of insurance’s complex pricing and how prices are inflated layer over layer in this system, let’s pause and ask, “Should they even be in insurance?”

Yes, that seems like a crazy question. But remember why we (really) want insurance. We want insurance if a medical need is both uncertain it might happen and if it is expensive. Cancer and chemo treatments- uncertain and expensive. Heart attack and coronary angioplasty – uncertain and expensive. These two pass the test. On the other hand, common cold and cough syrup - uncertain, but not expensive. It doesn’t make sense to throw this into the layer-cake.

What about pharmaceuticals? If you’re prescribed antihyperlipidemic agents for your high cholesterol, this is a chronic condition. Chronic meaning: persisting for a long time or constantly reoccurring. Sounds sadly predictable, doesn’t it? Ditto for the other most-prescribed pharmaceutical products in the U.S., such as beta-blockers (heart disease) or ACE inhibitors (high blood pressure).[2] Not uncertain.

Before we rush into pharmaceuticals being expensive or not, please consider other not-uncertain purchases in your life. How are they addressed. Amazon, I assume! The most popular products on Amazon’s “Subscribe and Save” listings, which could otherwise be labeled “Predictable Purchase Needs,” include things like paper towels, batteries, baby wipes, and detergent.[3] Consumers constantly need these items but are also able to price shop because they can plan ahead and buy them wherever they are cheapest-Walmart, Target, or their local grocery store.

What if predictable chronic care pharmaceuticals, often with generic substitutes, could be part of this broader price shopping and pre-ordering? Vitamins and probiotics, both daily personal health products, are in the top 10 Amazon “Subscribe and Save” products. If we could remove even some chronic, predictable pharmaceutical products from the insurance/PBM layer cake, lots of frosting/markups could be melted away, saving both money and lives.

As always, keep me updated on what you’re up to or reach out to chat with me about these issues!

Best,

TMD

[1] Kaiser Family Foundation has the dish on the full list of carve outs for pharmaceuticals.

[2] Top Prescription Drugs in the U.S. 2011-2014. Centers for Disease Control.

[3] Subscribe on baby wipes, save $2 on 12, and take preventive action on future diaper emergencies.